Weekly Outlook | Another busy central bank week

Important events this week:

– AU Interest Rate – Rates are anticipated to stay at 4.35% this month. The central bank upheld this rate in August, maintaining a hawkish outlook due to ongoing inflation above the 2-3% target. With a data-driven approach, the RBA is expected to keep policy tight until stability is achieved. Economic uncertainties loom, characterized by sluggish GDP growth, increasing unemployment, and global market volatility.

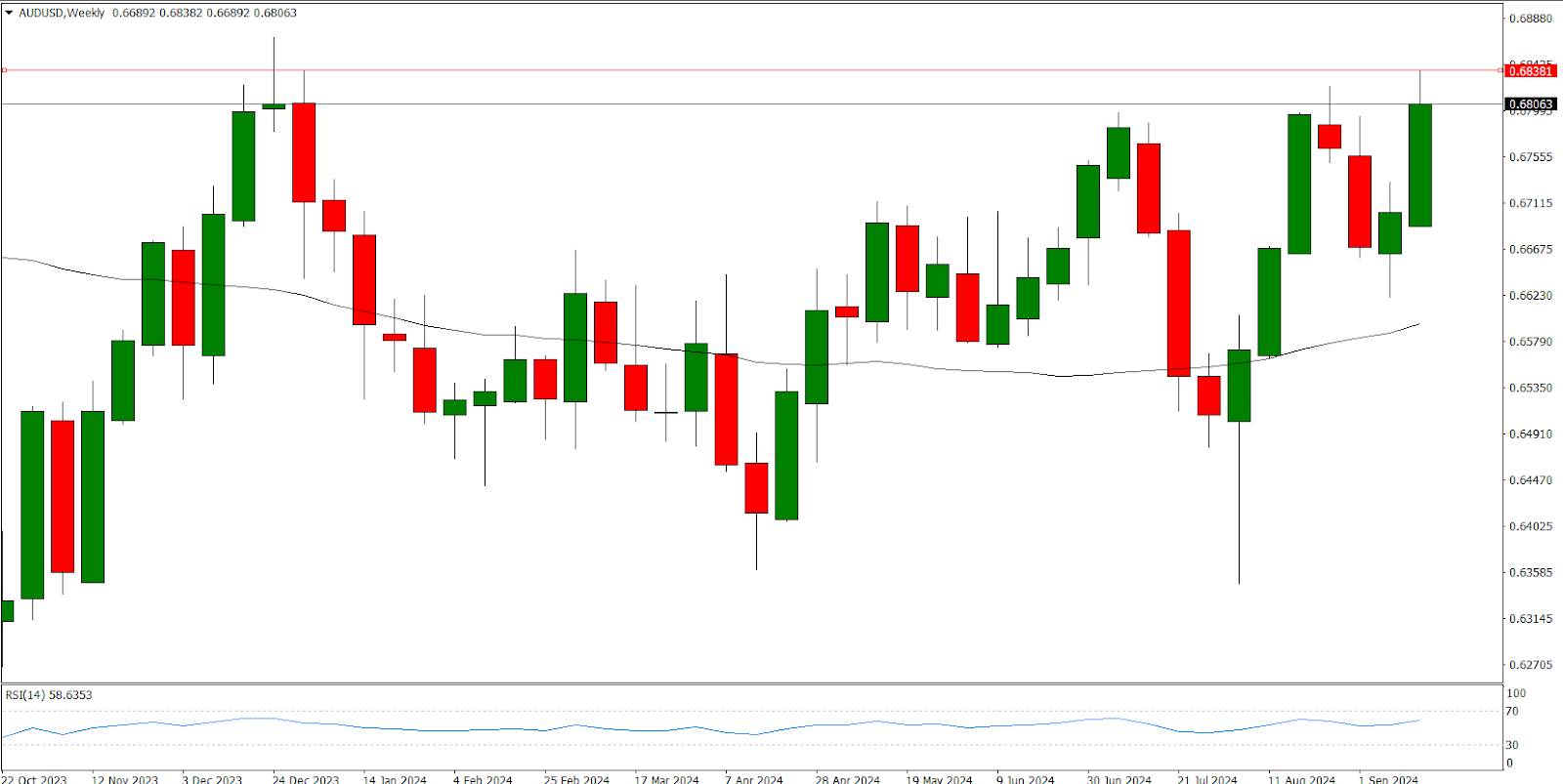

Based on the weekly chart above, in the previous week, AUD/USD surged by +117 pips, hitting a weekly high of 0.68387, largely driven by the Fed’s 50bps rate cut to 5%. The 50- period MA crossover indicates a bullish trend, but AUDUSD faces resistance at 0.6840, last tested in December 2023. A break above this level after the RBA’s rate announcement could signal further upside potential indicating a strong AUD, while a rejection could trigger a downside reversal indicating a weak AUD. The RBA will reveal its interest rate decision on September 24, 2024, at 6:30 CET.

– CH interest rate decision– The SNB is expected to announce a 25 bps cut to an interest rate of 1%, down from 1.25% in June. This would mark the third consecutive 25 bps reduction in 2024, following earlier cuts. Market expectations support this dovish stance, influenced by softening inflation and a robust CHF. The SNB maintains a 2024 inflation forecast of 1.3%, with GDP growth anticipated at 1% for the year and 1.5% in 2025.

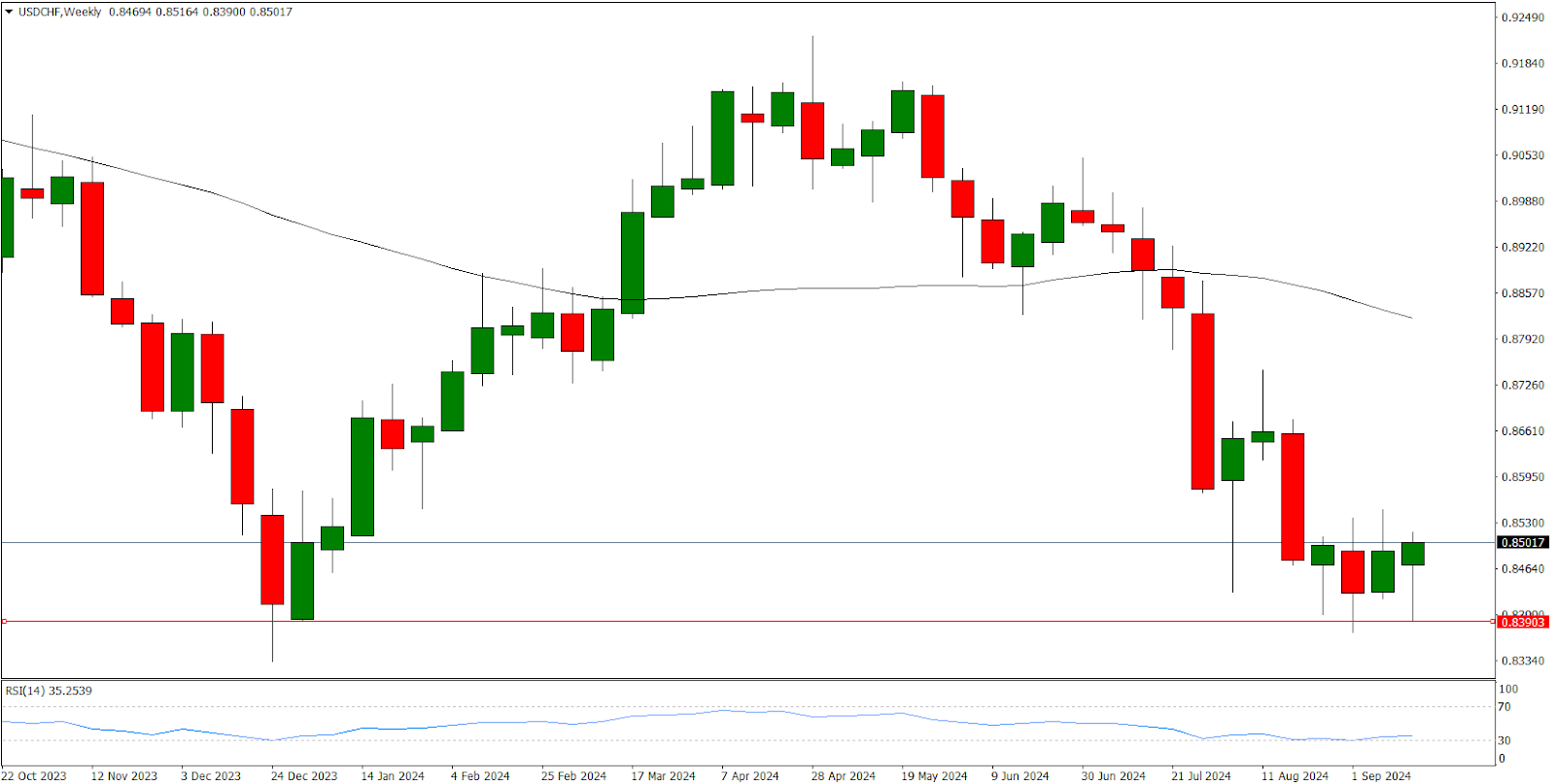

Based on the weekly chart above, last week, USDCHF rallied, adding 31 pips peaking at 0.8520 marking the week’s key support level after the Fed’s 50 bps cut. Although the pair trades below the 50-period MA, signaling potential downside, the key support at 0.8390 forming an uptrend since December 2023. A break below the support on the SNB’s potential rate cut could reinforce CHF strength, but a support bounce could shift momentum, signaling CHF weakness. The interest rate decision will happen on September 26, 2024, at 9:30 CET.

– CA monthly GDP –, the GDP data is expected to tick up from 0% to 0.1% following the BoC’s 25bps rate cut to 4.25%. Goods-producing industries shrank 0.4%, driven by drops in manufacturing and construction, partially cushioned by gains in utilities and agriculture. Manufacturing saw a 2.4% decline, its sharpest since Dec 2023, with durable goods hit by auto sector adjustments. Canada’s GDP is set for release on September 27, 2024, at 14:30 CET.

– US Core PCE Price Index – The price index is expected to hold steady at 0.2% MoM, matching August’s data and aligning with forecasts, continuing June’s 0.2% trend.

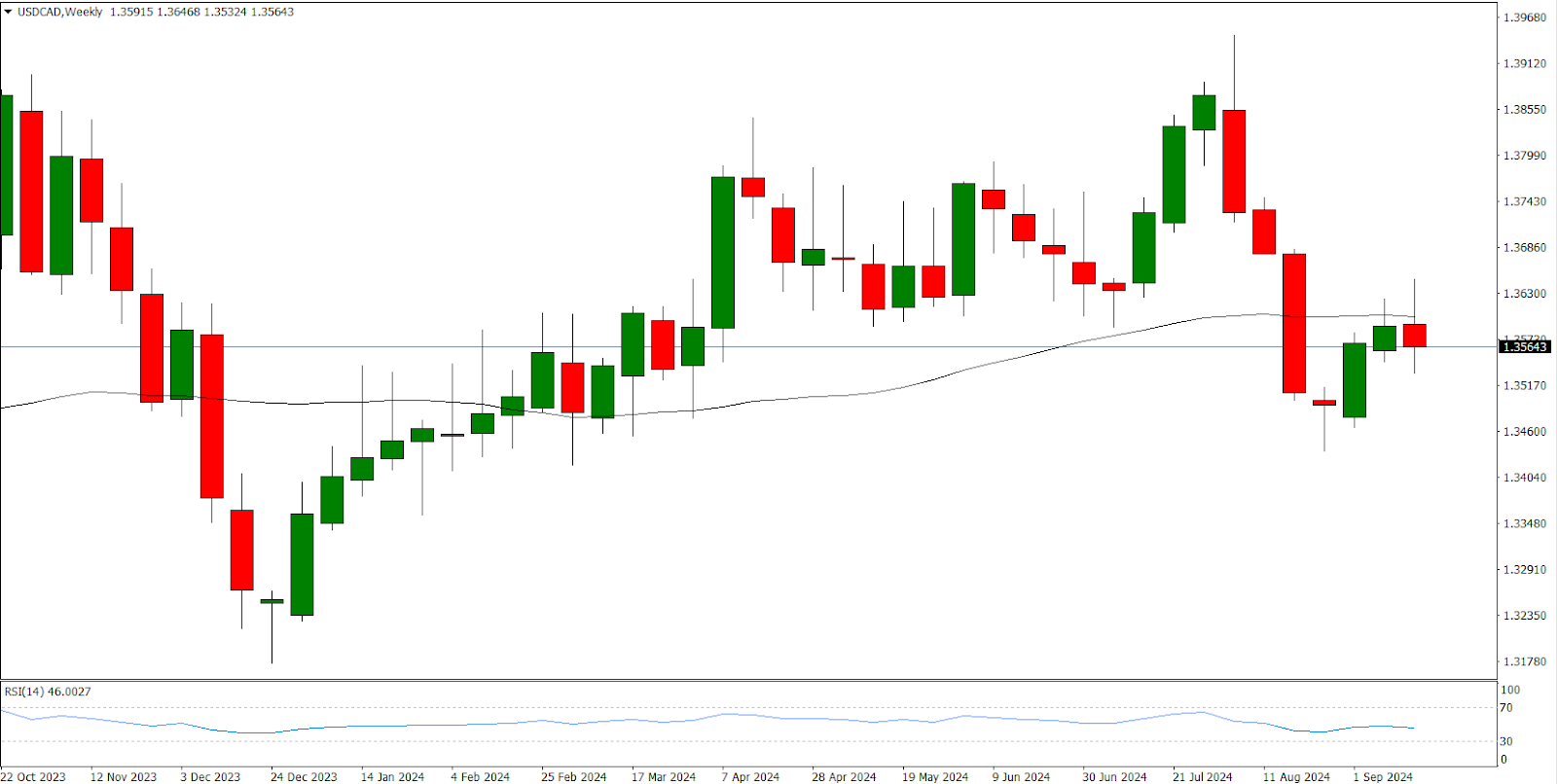

Last week, based on the weekly chart above, USDCAD shed 27 pips, ending with a weekly high at 1.36469 after the Fed’s 50bps cut. The pair currently trades below the 50-period MA after rejecting it, signaling potential downside continuation. If the 50-MA rejection holds, downside pressure may build, while a failure could suggest further upside momentum. The news event will be released on the September 27, 2024 at 14:30.