Tech and Nvidia bounce back, Dow pulls back

Headlines

* US Consumer confidence dips in June, USD steady

* Stronger than expected Canada CPI clips BoC rate cut bets

* Fed Governors reaffirm 2% inflation pledge but diverge on policy focus

* Gold slips as yields gain, markets await more US data

FX: USD finished marginally higher but off the recent highs around 105.90/91. US consumer confidence eased slightly from a downwardly revised May print. Fedspeak suggested rate setters will be in no rush to kickstart its rate cutting cycle.

EUR printed an inside day and settled lower just above 1.07. The recent swing low is at 1.0667. Eyes are on the first round of French election on Sunday. We’ve had soothing words from the National Rally about France’s budget trajectory. That has narrowed French/German yield spreads, but uncertainty is certainly evident.

GBP’s bounce off a Fib level at 1.2646 and 50-day SMA at 1.2632 saw it settle just below 1.27. BoE commentary has been curtailed due to next Thursday’s general election. Interestingly, both the UK and US money markets price in around 45bps of cut for 2024. That won’t very likely stay that way so that’s a pretty binary bet for positioning going forward.

USD/JPY had a very narrow trading day with prices hovering just below 160. Intervention alert is obviously very high after the Japanese authorities spent over $60 billion to help out the yen in late April and early May.

AUD again traded in a narrow range with prices trading around 0.6650. Focus turns to the inflation data today. CAD printed a doji after seven straight days of gains for the loonie versus USD. This comes after stronger than expected inflation data which eased July rate cut chances below 50%.

US Stocks: Equity indices were mixed with tech leading the upside in a change to the two prior days. The S&P 500 added 0.39% to 5,469. The Nasdaq 100 settled up 1.16%% at 19,701. In contrast, the Dow closed lower by 0.76% at 39,112, pulling back from a one-month high. Tech and communication services led the gains with real estate and materials the main laggards. Nvidia bounced back adding 6.8% and snapping a three-day losing streak. Walmart fell after the CFO flagged the second quarter as challenging while Home Depot dropped 3.6%.

Asian stock futures are mixed. Asian stocks were generally in positive territory. The mixed handover from the US markets where tech sold off held back more gains. The ASX 200 outperformed as energy and real estate led the way. The Nikkei 225 eventually made it to 39,000. The Hang Seng advanced with property stocks trumping tech weakness, while the mainland lagged.

Gold kept below the 50-day SMA at 2,340, but above strong support. Yields continued to track sideways with the 10-year US Treasury moving just above recent lows around 4.20%.

Day Ahead – Australia Inflation

The monthly CPI indicator is expected to tick higher to 3.8% from 3.6%. This month’s data will shed light on the unfolding of services inflation during the June quarter. Westpac analysts remind us that only 60% of the quarterly CPI is surveyed by the Monthly CPI Indicator. Many components are surveyed just one month each quarter, and some only once a year. That means it may not accurately reflect the quarterly CPI.

Analysts also say that this will be the first instance since September 2023 where the annual rate of inflation in the Monthly CPI Indicator surpasses that of the quarterly CPI. Regarding the RBA, the central bank kept to a hawkish tone at its recent meeting on inflation. It reiterated that inflation remains above target and is proving persistent, as it is moving more slowly than previously expected. Ultimately, the Board is not ruling anything in or out regarding rates.

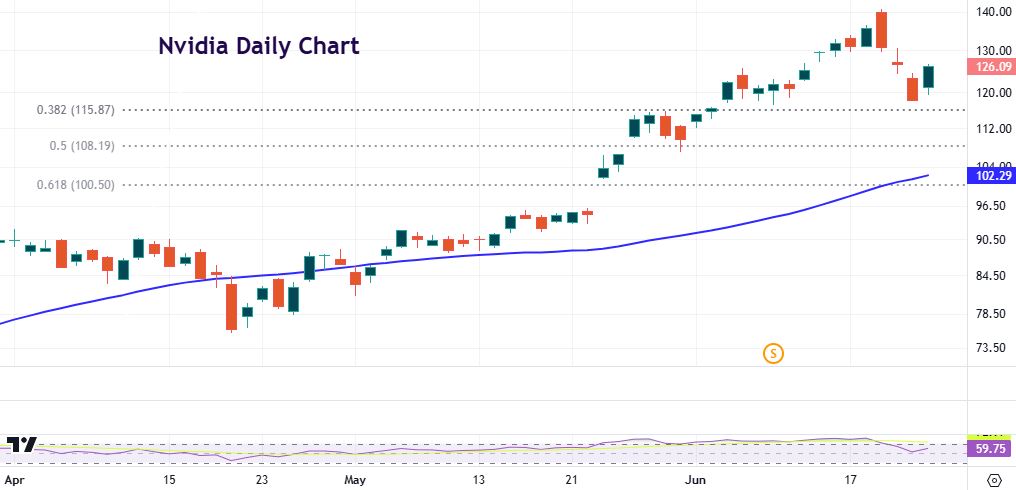

Chart of the day – Nvidia rebounds

The giant chipmaker was the world’s most valuable company last week. It moved above the perennial leaders, Apple or Microsoft, when it rose above $3 trillion in market cap. But that perch has been lost with Nvidia losing 13% in three days, down roughly $550 billion or 15% from last Thursday’s peak. The tech titan’s gains alone have been responsible for around a third of the benchmark S&P’ 500’s increase this year after it surged almost 140% in 2024. Will this spark a broader market slump? There have been similarities drawn with Cisco which lost 80% of its value in 2000-2001 during the dotcom bubble.

The 15% correction eased yesterday with a jump of nearly 7%, as the stock steadied just above the 38.2% Fib level of the April to June high move at $115.87. The all-time high sits at $140.76. The stock was trading some 20% above its 50-day SMA. That comes in at $102.29.