Tech rout, haven rally; next up ECB meeting

Headlines

* Trade fears hamper tech stocks, sell-off of winners intensifies

* Dollar tumbles on yen strength, sterling hits one-year high above 1.30

* ECB to hold rates as Europe prepares for summer break

* Gold drops off record high set on rate cut expectations

FX: USD broke down through recent lows to levels last seen in late March through 104. Carry trades unravelled with strength in havens offsetting any upside on the increasing odds of a Trump administration. In fact, Trump commented that the US had a “big currency problem” and that USD’s strength had hurt American competitiveness. Next support is 103.58, the halfway point of this years’ rally.

EUR jumped higher to levels from mid-March, through 1.09. The single currency has largely ignored Trump’s comments on tariffs that were aimed at the zone. The ECB meeting shouldn’t spring any big surprises as rate setters wait for more data and the September date for more policy action.

GBP pushed above 1.30 on marginally hotter than expected UK inflation data. Core prices were steady with services inflation stuck at a lofty 5.7%. August rate cut bets were reined in with now a 35% chance of a move versus 50:50 before the figures. The recent high is 1.3044.

USD/JPY dropped 1.35% with Reuters suggesting more intervention. Prices fell through the 50% point of the May low and recent top at 156.98. Trump highlighted the weakness in the yen as being advantageous for Japan.

AUD fell for a third day. Eyes are on the jobs data today. NZD/USD regained the 200-day SMA at 0.6074 despite softer than expected CPI data, as non-tradeable prices remained sticky. USD/CAD tracked sideways below 1.37. The BoC rate cut next week is virtually fully priced.

US Stocks: US markets generally fell with tech and semis leading the moves lower. The benchmark S&P 500 closed 1.39% lower at 5,588. The tech laden Nasdaq 100 finished off 2.94% at 19,799. The Dow Jones set record highs, closing 0.59% higher at 41,198.

Consumer staples and energy settled more than 1% higher, while tech slumped, off 3.72%. Semiconductor stocks got hit after Trump said Taiwan should pay the US for its defence. ASML didn’t help sentiment as it provided weak Q3 guidance.

Asian stock futures are in the red. Asian stocks were mixed Wednesday despite the positive mood Stateside with the S&P 500 and Dow Jones hitting fresh record highs. The ASX 200 was in the green with all-time highs in gold boosting related stocks. The Nikkei 225 saw gains reversed with the stronger yen potentially coming into focus. The Hang Seng and Shanghai Composite were muted amid Trump’s comments about trade frictions.

Gold made an intraday record top at $2483 before closing lower on the day. Treasury yields and the dollar closed lower too. Gold typically has an inverse relationship with the greenback and yields.

Day Ahead – Australia and UK Jobs, ECB Meeting

Australia employment is predicted at 20,000 in June, down from the prior May print of 39,700. The jobless rate is seen unchanged at 4%, with the participation rate marginally lower at 66.7%. Underemployment is one indicator the RBA will be watching. The job market is set to move below population growth with unemployment ticking higher through the year.

UK labour market tightness is very gradually fading though wage growth remains elevated. The unemployment figures, expected at 4.4%, have been clouded by statistical issues. The headline wage metric is forecast to cool to 5.7% from 5.9% and the ex-bonus measure to 5.7% from 6%. BoE August rate cut bets have eased after still high services inflation data released yesterday.

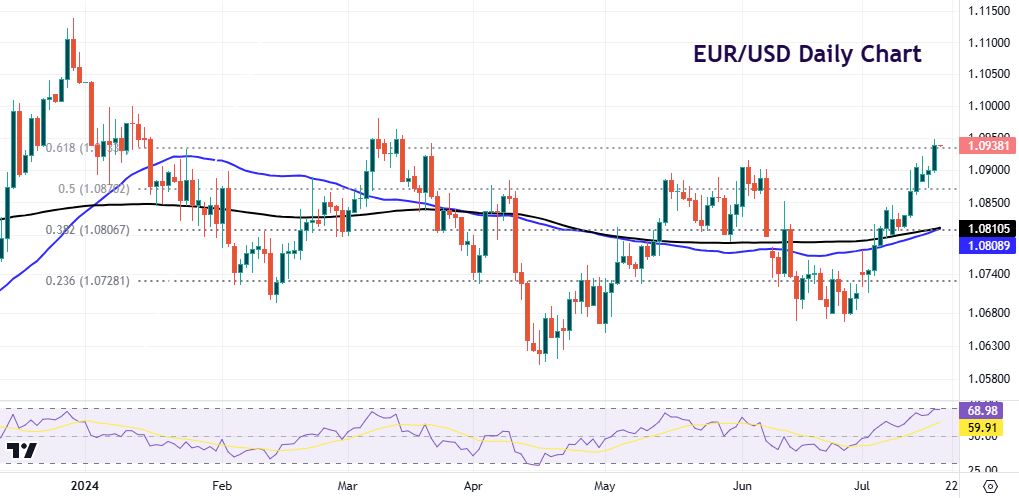

Chart of the day – EUR/USD looking bullish into ECB

The ECB meeting is expected to be a “nothingburger” as we said in our weekly preview. We are likely to hear that policymakers are data dependent and continue to have a meeting-by-meeting approach. President Lagarde has already highlighted this is a summer meeting and that wage data and productivity will be key going forward. Current market pricing sees 48bps of rate cuts for 2024 with a September move nailed on. We also get fresh ECB staff economic projections published at the next meeting in mid-September.

A pushback on a “normal” rate cutting cycle, perhaps a “hawkish hold”, could boost the euro and push it decisively beyond the March highs at 1.0981 and beyond. But explicitly lining up another rate reduction in September could hit the single currency.